Blockchain technology is a revolutionary innovation that has the potential to transform various industries. It’s a distributed, immutable, and transparent ledger that records transactions across a network of computers. This technology is gaining traction because it provides a secure, efficient, and verifiable way to track and manage information.

Introduction

Blockchain technology is essentially a digital ledger that records transactions in a secure and transparent way. Each block in the chain contains a collection of transactions that are verified and then added to the chain. Once a block is added, it cannot be altered or removed, ensuring the integrity of the data. This decentralized nature, coupled with the cryptographic security, makes blockchain a powerful tool for various applications.

This technology is gaining immense popularity due to its potential to revolutionize various industries. From finance and supply chain management to healthcare and voting systems, blockchain’s impact is being felt across the board. But what exactly is this technology, and how does it work? Let’s delve into the intricacies of blockchain, exploring its key features, applications, and implications.

What is a blockchain?

A blockchain is a distributed, immutable ledger that records transactions in a secure and transparent way. It is essentially a chain of blocks, each containing a set of transactions. These blocks are linked together in chronological order, creating a tamper-proof record of all transactions.

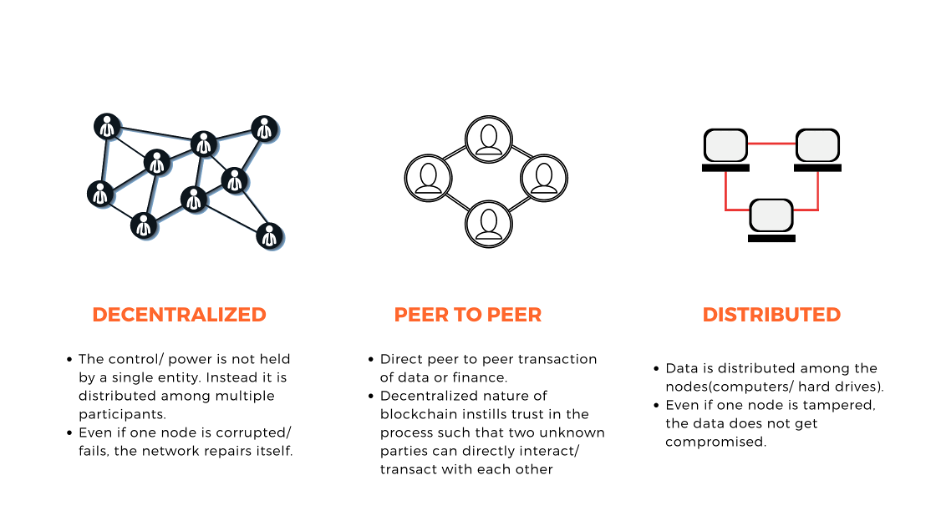

- Distributed ledger: The blockchain is not stored in a single location but is distributed across a network of computers. This decentralized nature makes it very difficult to tamper with the data.

- Immutable: Once a transaction is recorded in a block, it cannot be altered or deleted. This ensures the integrity of the data and provides a trustworthy record of transactions.

- Transparent: All transactions on the blockchain are publicly viewable. Anyone can access the ledger and verify the authenticity of transactions.

- Secure: Blockchain uses cryptography to secure transactions and protect the data from unauthorized access.

- Decentralized: There is no central authority controlling the blockchain. This makes it resistant to censorship and manipulation.

How does blockchain work?

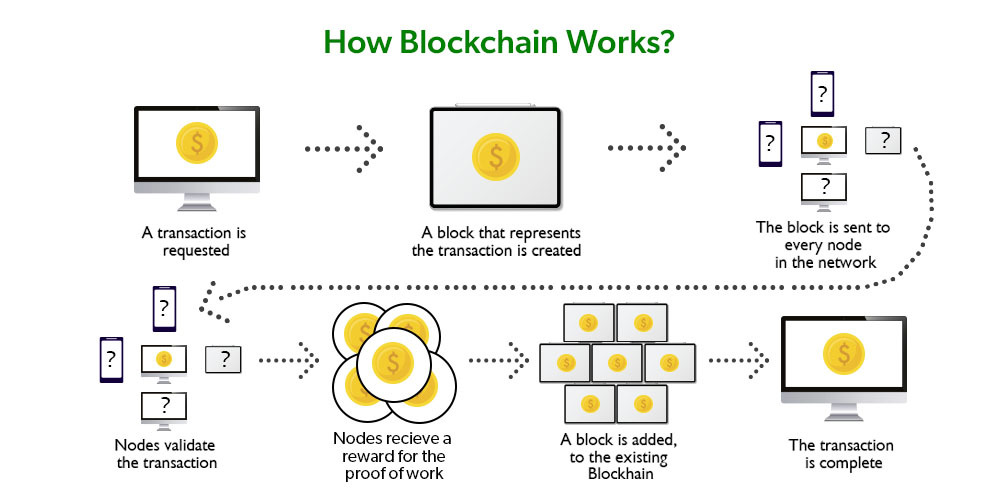

The blockchain operates on a principle of consensus, where all participants in the network agree on the validity of transactions. This is achieved through a process called mining.

- Mining: Miners are computers that solve complex mathematical problems to verify transactions. The first miner to solve the problem gets to add the next block to the chain and is rewarded with cryptocurrency.

- Consensus: Once a block is added to the chain, all other participants in the network validate it. This ensures that all nodes have the same version of the blockchain and that the data is consistent.

- Smart contracts: Blockchain can also be used to execute smart contracts, which are self-executing agreements that automatically enforce the terms of a contract. This eliminates the need for intermediaries and can automate various processes.

- Tokens: Blockchain technology is often associated with cryptocurrencies, such as Bitcoin and Ethereum. These are digital assets that are secured and managed using blockchain.

Applications of blockchain technology

Blockchain technology has a wide range of applications across various industries. Here are some of the most prominent examples:

- Finance: Blockchain can be used to streamline financial transactions, improve security, and reduce costs. For example, it can be used for cross-border payments, asset management, and trade finance.

- Supply chain management: Blockchain can be used to track goods and products throughout the supply chain, ensuring transparency and accountability. This can help to prevent counterfeiting, improve efficiency, and reduce waste.

- Healthcare: Blockchain can be used to secure patient records, improve data sharing, and facilitate clinical trials. It can also be used to track pharmaceuticals and prevent fraud.

- Government: Blockchain can be used to improve the efficiency and security of government processes, such as voting, identity management, and land registration.

The future of blockchain technology

Blockchain technology is still in its early stages of development, but it has the potential to transform many industries. As the technology continues to evolve, we can expect to see even more innovative applications of blockchain.

- Interoperability: The development of interoperable blockchain platforms will allow different blockchains to communicate with each other, expanding the possibilities for collaboration and innovation.

- Scalability: The ability to process a higher volume of transactions on the blockchain will be crucial for widespread adoption.

- Regulation: Clearer regulatory frameworks for blockchain technology will be essential for building trust and confidence in the technology.

- Integration with existing systems: The integration of blockchain technology with existing systems will be essential for seamless adoption.

Conclusion

Blockchain technology is a powerful tool with the potential to revolutionize various industries. Its key features – immutability, transparency, and security – make it an attractive solution for a wide range of applications. As the technology continues to evolve and mature, we can expect to see even more innovative use cases emerge.

From streamlining financial transactions and securing patient records to tracking products in the supply chain and improving government processes, blockchain has the potential to transform the way we do business and live our lives. As we move forward, it’s important to stay informed about the latest developments in this exciting and rapidly evolving technology.